For a long time, tokenized securities trading felt like one of those ideas the market liked to talk about more than actually implement. The promise was always clear, but the infrastructure, regulation, and market confidence were not yet fully in place.

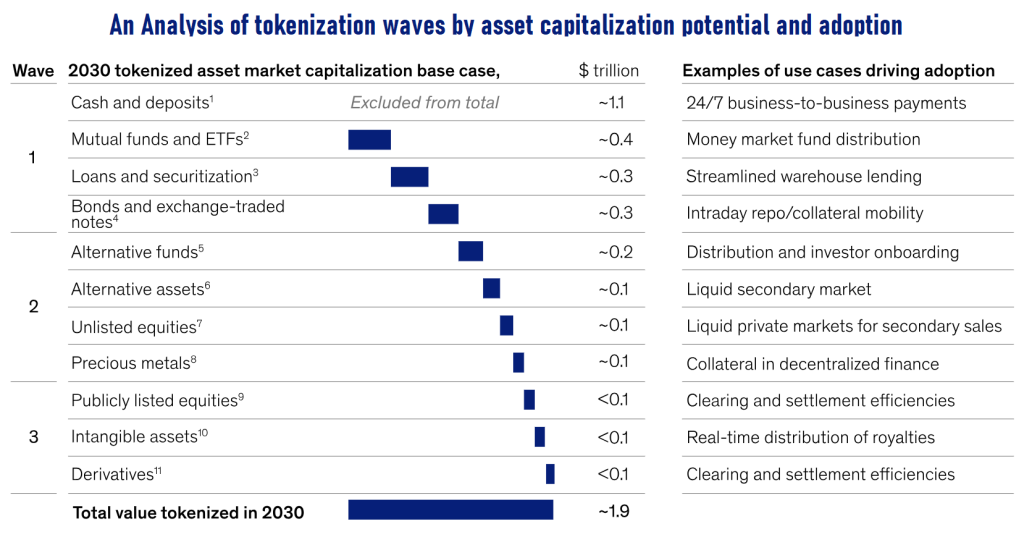

That is why 2026 feels different. The SEC has now approved Nasdaq’s framework for tokenized trading and settlement of certain securities, which moves the conversation from theory to actual regulated market infrastructure. From where I sit, that shift matters because this is no longer just about innovation headlines. It is about whether capital markets can start using blockchain in a practical, regulated, and large enough way to matter. McKinsey estimates tokenized market capitalization could reach around $2 trillion by 2030, which tells me this space is no longer being treated like a side experiment.

What is Tokenized Securities Trading and Why Does it Matter in 2026?

Tokenized securities trading is simply the trading of regulated assets like stocks or ETFs in token form on blockchain-based infrastructure. The important part is that the asset may look different technically, but it is still the same security from a legal and market perspective. The SEC made that clear in 2026: tokenized securities are still securities, which means the rules do not disappear just because the format changes.

Why does that matter now? Because the market has started moving past theory. DTCC’s initial tokenization scope includes the Russell 1000 and major index ETFs, which means this is being tested around some of the most important and liquid parts of the U.S. market, not around fringe assets. That is why I see 2026 as a serious turning point. The conversation is no longer “Can tokenized securities exist?” It is “how do we make them work inside real market infrastructure?

This shift from theory to execution is similar to what we’re seeing across AI adoption, where technologies move from experimentation into real workflows.

How Tokenized Securities Trading Works in Regulated Markets

On the surface, tokenized securities trading may sound like a completely new kind of market. In practice, the current model is much more controlled than that. What makes it interesting is not that it replaces regulated market structure overnight, but that it starts introducing blockchain-based settlement into a system investors already know.

Trading on the same exchange

Tokenized securities do not begin in a separate crypto-style venue. They trade within the same regulated exchange environment, which keeps the process familiar and avoids creating a parallel market just for blockchain-based versions of securities.

Using the same order book

The tokenized version of a security sits on the same order book as the traditional version. That means both formats are meant to follow the same pricing logic, the same execution priority, and the same market treatment.

Executing the trade first

The trade itself happens through the normal exchange workflow. This is important because tokenization does not change how the order gets matched. It becomes relevant only after the trade is already executed.

Choosing a tokenized settlement

Eligible participants can choose a tokenized settlement by using a specific instruction at order entry. That instruction tells the system that, once the trade is complete, it should move through the tokenization route rather than remain fully on the traditional settlement path.

Passing through the DTC infrastructure

After execution, Nasdaq passes the settlement instruction into the post-trade layer, where DTC handles the tokenization side. This is one of the biggest reasons the framework matters, because it connects tokenization to real market infrastructure instead of leaving it as a side experiment.

Keeping the same investor rights

The tokenized security is still meant to carry the same core rights as the traditional security. The ticker, legal treatment, and shareholder protections are not supposed to change just because the asset is represented in token form.

Using a fallback mechanism

If tokenized settlement cannot be completed because of a technical issue or an eligibility problem, the trade does not fail. It falls back to the traditional settlement route, which makes the structure more practical for real markets where reliability matters more than novelty.

Operating within T+1 settlement

Even with tokenization in the workflow, the current model still follows a T+1 settlement structure. That is why I see this as a serious step forward, but not the finished version of on-chain securities markets.

Why Nasdaq’s Move Changes the Conversation Around Tokenized Securities Trading

Nasdaq’s move matters because it takes tokenized securities trading out of theory and places it inside a regulated exchange framework. That changes the discussion from “is this possible?” to “how does this get adopted in real markets?” Reuters reported that the SEC-approved setup allows certain tokenized securities to trade alongside traditional shares under the same market structure.

- It brings tokenization into a regulated market, not just private pilots.

- It treats tokenization as an infrastructure upgrade, not a new asset class.

- It keeps the same ticker, pricing logic, and investor rights, which makes the shift more practical for institutions.

- It becomes more credible because DTC is part of the post-trade flow, not just a blockchain platform on the side.

- It starts with assets tied to the Russell 1000 and major ETFs, which shows this is being tested in serious market segments.

That is the real signal. Nasdaq’s move does not mean the market is fully on-chain yet, but it does mean tokenized securities trading is now being treated as part of real market infrastructure, not just a future concept.

Key Benefits of Tokenized Securities Trading for Issuers, Investors, and Market Infrastructure

Tokenized securities trading is getting real attention now because the value is not just digital packaging. The real upside is operational. Once tokenization is built into market infrastructure, it can improve settlement, servicing, and how securities move across the financial system.

Faster settlement

One of the biggest benefits is the potential to reduce delays in post-trade movement. Even when markets are not fully instant yet, tokenized infrastructure moves the system closer to faster and more flexible settlement models.

Better collateral

Tokenized securities can make collateral more mobile and more usable. That matters because a lot of value in financial markets gets trapped in slow post-trade processes, and tokenization can help make that capital easier to deploy.

Lower friction

A tokenized structure can reduce manual steps across settlement, reconciliation, and asset servicing. That does not sound flashy, but this is exactly where real market efficiency usually comes from.

More automation

Smart contract-based workflows in enterprises create room for more automation around processes like lifecycle management, reporting, eligibility checks, and margin-related actions. That makes the infrastructure more responsive and less dependent on heavy operational work.

Greater transparency

Tokenized market infrastructure can improve record visibility and traceability across transactions and ownership movement. For institutions, this creates a stronger base for control, auditability, and cleaner operational oversight.

Broader access

Over time, tokenization can support wider distribution and more flexible participation models across markets. That does not mean access becomes frictionless overnight, but it does create a better foundation for more connected and globally reachable capital markets

Common Challenges in Tokenized Securities Trading that the Market Still Needs to Solve

- Legacy systems still slow things down. Tokenization sounds modern, but most firms still have to make it work with older custody, settlement, and reporting infrastructure.

- Interoperability is still weak. A tokenized security loses value quickly if it cannot move smoothly across platforms, custodians, and market systems.

- Liquidity is not automatic. Putting a security on-chain does not guarantee active secondary trading or deeper market participation.

- Regulation is clearer, but not easy. Broadridge found that 73% of financial institutions see regulatory uncertainty and legal risk as the biggest challenge to scaling tokenized offerings.

- Security still matters. Wallets, smart contracts, and digital asset controls all need to work properly, or trust breaks fast.

- Market readiness is still uneven. A lot of firms like the idea of tokenization, but far fewer are ready to support it operationally at scale.

Also Read: Is the India AI Summit the Catalyst We’ve Been Waiting For?

Tokenized Securities Trading vs Traditional Securities Trading: What Actually Changes?

The easiest mistake here is to assume that tokenized securities trading creates a completely different market. It does not. In the current regulated model, a lot stays the same on purpose. The real shift is happening in the infrastructure layer, especially around how ownership can be represented and how post-trade workflows can evolve. The SEC has also been clear that tokenized versions of securities remain subject to securities regulation.

| Area | Traditional securities trading | Tokenized securities trading |

|---|---|---|

| Trading setup | Trades through existing exchange infrastructure. | In the current model, it still trades inside the same regulated market structure. |

| Settlement model | Uses traditional clearing and settlement rails. | Adds a tokenized settlement layer, but still depends on regulated post-trade infrastructure. |

| Asset format | Ownership is recorded in the usual market system. | Ownership is represented in token form, while the security itself remains the same. |

Why Tokenized Securities Trading Still Needs Compliance, Custody, and Market Structure

One mistake I keep seeing is the idea that once a security is tokenized, the hard part is done. No, it’s not. A tokenized security still has to follow the same legal and regulatory standards, which is exactly why the SEC made it clear in 2026 that tokenized securities are still securities under federal law.

Custody is just as important. In regulated markets, ownership, control, and entitlement cannot be left unclear just because the asset is now in token form. That is why tokenized trading still depends on trusted custody and post-trade infrastructure, not just blockchain rails on their own.

Market structure matters for the same reason. Trading is only one part of the system, while clearing, settlement, servicing, and operational trust are what make the model usable at scale. DTCC has pointed to tokenization’s potential to unlock up to $100 billion in industry-wide efficiencies, but that value only becomes real when the full market structure around it is dependable.

How Regulation is Shaping the Future of Tokenized Securities Trading

What makes this stage interesting is that regulation is no longer only reacting to tokenization. It is starting to shape the rules of the model itself. The SEC’s 2026 guidance does more than say tokenized securities are still securities. It starts drawing clearer lines around structure, especially between issuer-sponsored tokenized securities, third-party entitlement models, and synthetic exposure products. That matters because the future of this market will depend on how clearly firms define what they are actually issuing, what rights the holder really has, and how ownership is recorded.

- It is pushing the market to define what kind of tokenized product is being offered.

- It is forcing firms to be clearer about investor rights and ownership records.

- It is moving adoption toward a controlled, standards-based infrastructure instead of loose experimentation.

- It is making regulators look more closely at issuance, trading, and post-trade policy gaps that still need answers.

- It is encouraging a phased rollout, which is sensible when the U.S. equity market plumbing already supports more than $1.9 trillion in daily trading volume.

This growing role of regulation and trust is not unique to finance; it is becoming a defining factor across AI-driven industries like Healthcare, Education, Hospitality, and more.

What Comes Next for Tokenized Securities Trading in Global Capital Markets?

What comes next is unlikely to be a sudden shift where capital markets move fully on-chain all at once. The more realistic path is phased and infrastructure-led: stronger post-trade tokenization, clearer ownership models, tighter custody standards, and broader adoption in the parts of the market where the operational value is easiest to prove first. That direction is already visible. DTCC has said digital cash settlement is part of the next stage of exploration, suggesting the long-term opportunity.

As the founder of TechnoBrains, I believe the next phase of tokenized securities trading will be shaped less by who launches first and more by who builds something the market can actually rely on. In financial infrastructure, novelty does not win on its own. What lasts is what can operate under regulatory scrutiny, fit into real workflows, and hold up under real market pressure.

Tokenized securities trading is still early, but it is clearly moving beyond the concept stage. The firms that treat it as serious market infrastructure, rather than just a digital trend, will be the ones best positioned for what comes next.

If you are interested in how emerging technologies like tokenization, AI, and digital infrastructure are shaping real-world markets, you can explore more insights, where I regularly share perspectives on technology, product strategy, and market shifts.